Profile

Legal Structure

A. Rahim Foods (Pvt.) Limited (‘A. Rahim Foods’ or ‘the Company’) is an unlisted Private Limited Company, incorporated in 1987, under the erstwhile Companies Ordinance, 1984 (now the Companies Act, 2017). The Company’s registered office is located in Lahore.

Background

The

first Dawn plant was set up and commissioned in Karachi in October 1981 with

the purpose of creating awareness and demand for a variety of bread products.

It was not long before the name became synonymous with ‘Vitamin Enriched Bread’

and a second plant was commissioned in Islamabad in 1985. Since then, Dawn has

done many accomplishments; It has managed to capture 35% of the consolidated

market share of all bread products in Pakistan within a decade of inception.

Operating for nearly 4 decades, Dawn Bread is the only brand in Pakistan that

delivers freshly baked bread in its 3 provinces. The group has further

diversified with Dawn Foods (a frozen foods manufacturer), ATA Bakery Solutions

(a producer of premium bakery products) and the

recently established international brand, Doughstory (a manufacturer and

exporter of frozen food and bakery products). AB Mauri Pakistan (Private)

Limited (Manufacturer of Yeast) is, a joint venture of AB Foods International

and A Rahim Foods, devoted to the baking industry engaged in yeast and bakery ingredients.

Operations

The Company's operations are primarily focused in the Punjab region, and it boasts one of the largest delivery fleets in Pakistan, with over 1,000 vehicles. Serving more than 150 cities nationwide, the company efficiently reaches every retail store that wishes to carry its products. The production plants are located in Lahore (Kot Lakpat) and Muridke. The total annual production capacities for each product are as follows: 354.7 million units for buns and burgers, 109.3 million units for bread, 10 million units for rusks, 10 million units for muffins and cakes, and 80.3 million units for bread.

Ownership

Ownership Structure

The Company’s ownership is split between two members, Mr. Anwaar Hussain and his brother Mr. Noman Hussain. Constituting 50% each.

Stability

A. Rahim Foods is family owned. Both brothers hold strong ties, as they have jointly led the Company to its present stage. Further, family engagement under a well designed integrated plan may be needed.

Business Acumen

The sponsors bring extensive experience and expertise in the food and bakery industry. Their sound business acumen has been instrumental in driving the Company’s sustained success over the years. With deep industry-specific knowledge, hands-on experience, and strategic foresight, the sponsors have played a key role in shaping the Company’s growth and long-term achievements.

Financial Strength

The Company has successfully diversified into various food segments. Additionally, the Company draws its financial strength from its group entities, including Dawn Frozen Food, ATA Bakery, and ARF itself.

Governance

Board Structure

The Board is not truly independent of the management. The Board of the Company is composed of two members, including the Chief Executive Officer (CEO). Both members serve as Executive Directors, actively involved in the day-to-day management and strategic decision-making of the Company.

Members’ Profile

Mr. Anwaar Hussain- CEO

and Director has been managing

the affairs of Dawn Foods Group for the last 20 years. With his

expertise and diversified

experience, he successfully expanded the Group into

multiple industries with success

stories in frozen food and ambient carbohydrate businesses, including the largest

distribution network in Pakistan that consists of a country-wide network of 30 warehouses.

Mr. Noman Hussain, has been managing the affairs of

Dawn Group for last 18 years as a Group

Director. Mr. Noman holds a MBA in Business Administration and Management, from the University of Connecticut, USA.

Board Effectiveness

The Company has yet to establish formal board committees, which presents an opportunity for further enhancement in its governance structure. The Board meets on an annual basis, though formal minutes of the meetings are not documented.

Financial Transparency

The External Auditors of the Company M/S Crowe Hussain Chaudhry &

Co. Chartered Accountant a QCR-rated firm expressed an unqualified opinion of

Financial Statements for the period ended Jun’24. The Firm is Category ‘A’ on

SBP panel.

Management

Organizational Structure

The

Company employs a horizontal organizational structure, with each department

managed by department heads reporting directly to the Executive

Directors. The Company functions across 9

key areas: (i) Admin, (ii) Sales, (iii) Marketing, (iv) Supply chain, (v)

Finance, (vi) R & D, (vi) Quality, (vii) Human Resource and (viii) Technical & (ix) Quality. Mr. Anwaar Hussain, the CEO, oversees the Sales,

Finance, Human Resource, Supply Chain, and Marketing departments. Mr. Noman, on

the other hand, leads the R&D, Quality, Technical, Administration, and Information

Technology departments.

Management Team

Mr. Anwaar Hussain serves as the Chief Executive Officer (CEO) of the Company. A seasoned professional and a distinguished member of the Young Presidents' Organization (YPO), Mr. Anwaar brings a proactive and dynamic approach to his role. With extensive industry experience and a deep understanding of the sector, he effectively inspires and leads the team. The CEO is supported by a team of highly experienced professionals.

Mr. Noman Hussain has been overseeing the operations of the Dawn Group for the past 18 years in his role as Group Director. He holds an MBA in Business Administration and Management from the University of Connecticut, USA.

Mr. Harris Mahmood, FCA, serves as the Group

Chief Financial Officer, overseeing the Strategy, Finance, Legal, Internal Audit, and Information Technology functions across the group. This includes 100% owned legal entities in multiple countries, as well as global and local joint ventures. Mr. Harris brings over 20 years of overall experience.

Effectiveness

There

are currently no formal management committees in place. However, the management

team convenes its meeting on monthly basis to ensure the

efficiency and effectiveness of the Company's operations.

MIS

The

Company utilizes SAP software, a specialized ERP

solution designed for manufacturers and tool producers. The software is

continuously monitored and maintained by the vendor to ensure optimal

performance.

Control Environment

The Company has a robust internal audit function outsourced to EY Ford Rhodes, which enhances risk management, control, and governance processes, while driving continuous business improvements through the development of Standard Operating Procedures (SOPs). Additionally, the Company holds several prestigious certifications, including HACCP, Halal, FDA, ISO 9001, ISO 22000, and Kosher, demonstrating its strong commitment to adhering to the highest industry standards of quality, safety, and compliance.

Business Risk

Industry Dynamics

In Pakistan, the convenience food market is primarily dominated by domestically produced products. This industry is highly competitive, with products that are particularly sensitive to price fluctuations. A significant portion of the market is also held by unbranded products, which play a notable role. Production of food groups increased by 1.7 percent in FY24, compared to a contraction of 7.1 percent in FY23. Where the sugar confectionary market covering 20% exports of Prepared Foodstuffs; Beverages, Spirits, Vinegar and Tobacco, showed the growth of 13.9% during FY24 compared to 8.9% during FY23. The food sector in Pakistan is experiencing rapid growth, driven by population increase, inflation, urbanization, and evolving consumer lifestyles.

Relative Position

The Company has established strong brand recognition in the bread and buns industry, with its flagship products, "Dawn Bread" and "Dawn Burger Buns," becoming widely recognized for their quality and reliability. The Company has

managed to capture ~35% of the consolidated market share of all bread products

in Pakistan within a decade of inception.

Revenues

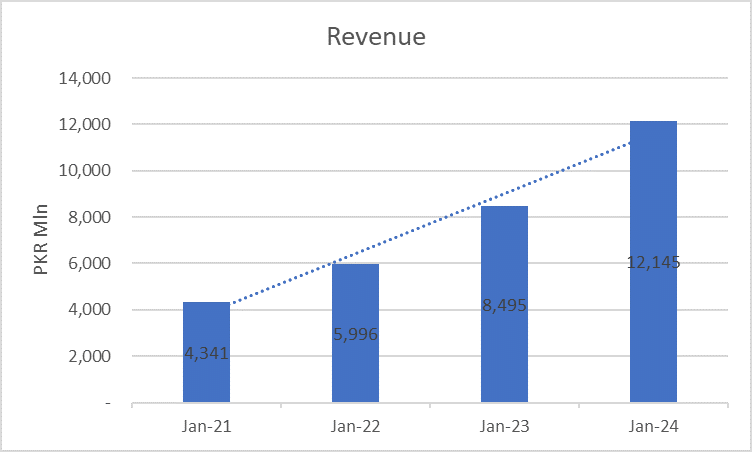

A. Rahim Foods, a prominent player in the food processing and distribution sector, has consistently demonstrated revenue growth and successfully navigated market fluctuations, maintaining a strong financial position. The Company's revenue is derived from seven product segments, including bread, buns, burgers, flatbread, frozen paratha, rusk, and sweet cakes/ muffins. Bread constitutes ~48% of the Company’s total revenue, with burgers contributing ~36%, cakes/ muffins contributing ~9% followed by rusk ~4 and others ~3%, reflecting their essential role in the Company’s overall financial performance. The Company saw a positive trend in its topline, driven by higher sales volumes and increased prices. In FY24, the Company achieved total revenue of PKR 12bln (FY23: PKR 8bln), representing an impressive increase of ~42%.

Margins

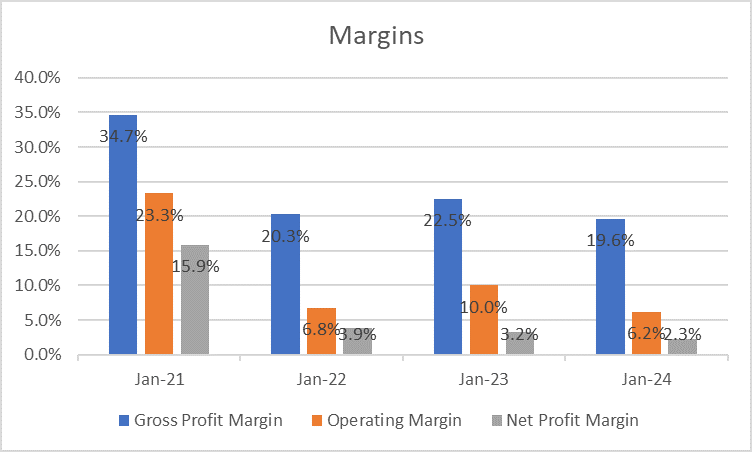

During FY24, the gross profit margin decreased to 19.6% from 22.5% compared to the previous year, primarily due to rising raw material and energy costs and a challenging market environment. This trend was further reflected in operational activities, as operating expenses surged by 54.5%, increasing from PKR 1,059 million in FY23 to PKR 1,637 million in FY24, primarily driven by higher selling and marketing expenses. As a result, operating profit margins contracted to 6.2% in FY24, compared to 10% in FY23. The cumulative impact of these factors led to a reduction in net profit margins, which fell to 2.3% from 3.2%. Net profit reached PKR 282 million in FY24, a modest increase from PKR 275 million in FY23. This improvement was also supported by a slight reduction in finance costs due to lower borrowings. The Return on Equity (ROE) remained relatively stable at 10.3% in FY24, compared to 10.7% in FY23, reflecting consistent performance in generating returns on shareholders' equity. Overall, while the Company remained profitable, it faced significant cost pressure that impacted its margin performance. The margins have improved in the ongoing financial year, as represented by the management.

Sustainability

The Company has shown growth trajectory

since its inception and now the drive towards the future is stronger.

Financial Risk

Working capital

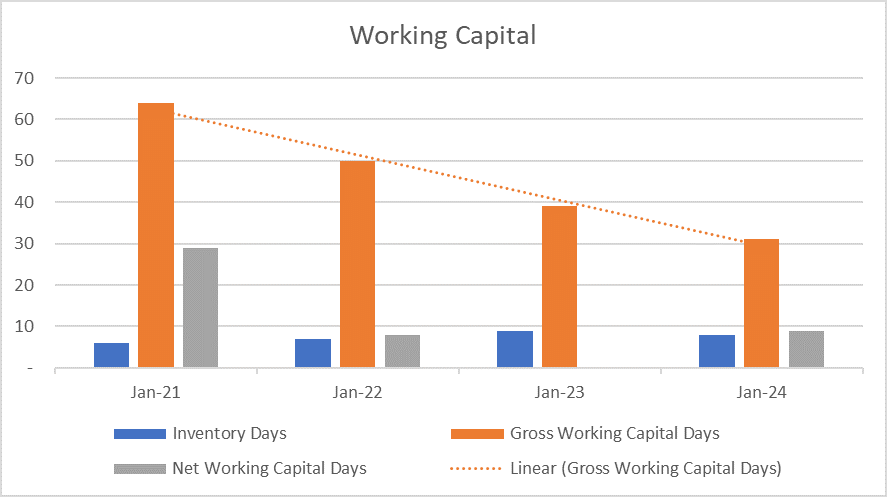

A. Rahim Foods’ working capital requirements are driven by its inventory, trade receivables, and trade payables, and are financed through short-term borrowings and free cash flow from operations (FCFO). In FY24, the average inventory days slightly improved, reducing to 8 days in FY24 from 9 days in FY23, indicating efficient inventory management and optimized stock levels to balance demand with minimal holding costs. Trade receivable days remained negligible at 24 days on average, reflecting the company’s efficient receivables collection practices.This led to improved Gross working capital days at 31 days (FY23: 39 days). However, trade payables stood at 23 days, lower than in the previous period (FY23 38 days). These contributed to a net working capital cycle of 9 days. The current ratio stood at 1.6, compared to 1.3 in the previous period, indicating improved liquidity and a stronger ability to meet short-term obligations. Overall, the results suggest that the Company has made progress in streamlining its working capital, although there remain areas for continued improvement in managing payables and receivables more efficiently.

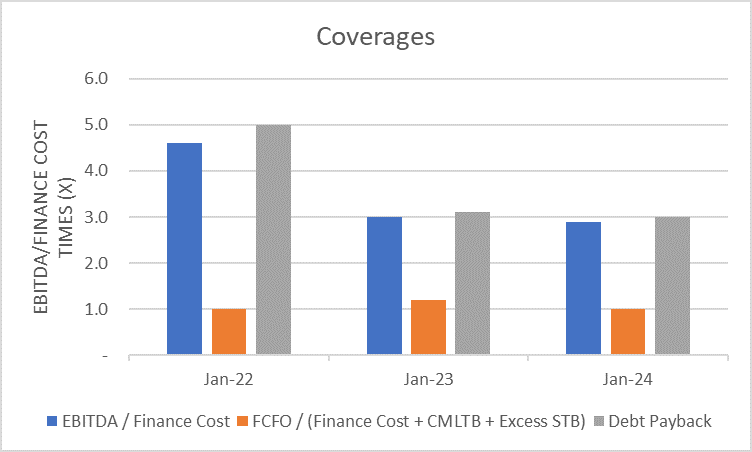

Coverages

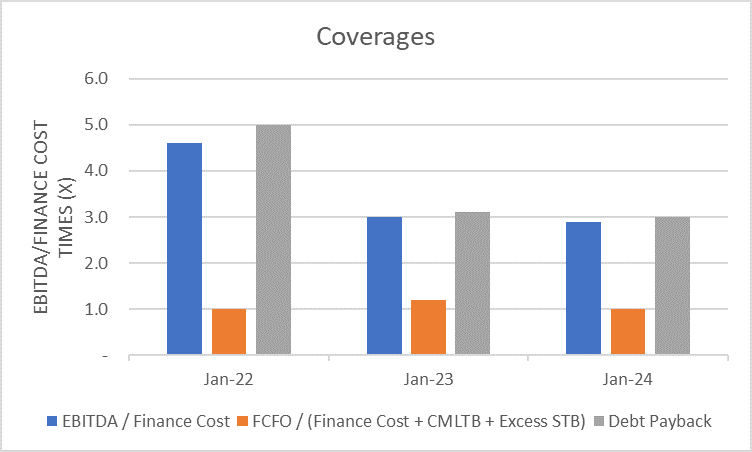

The EBITDA-to-Finance Cost

ratio slightly increased to 3.6x (FY23: 3.4x), signaling a increased capacity to cover finance

costs through operational earnings. The FCFO-to-Finance Cost ratio has

weakened to 2.9x from 3.0x, indicating tighter cash flow coverage of financial

obligations. T he Company’s Free Cash Flow from Operations (FCFO) decreased by 3.8%, dropping from PKR 1,127 million in FY23 to PKR 1,084 million in FY24 due to increase in taxes paid. This decline in operational cash flow, however, still reflects the Company’s adequate operational performance and cash generation capacity. The Company’s financial health is further demonstrated by a debt payback ratio of 3.0x, signifying a solid ability to manage and reduce its debt obligations effectively.

Capitalization

The

Company maintains a moderately leveraged capital structure, with a consistent

leverage ratio of 49.3% in FY24, reflecting a prudent borrowing strategy. As of

FY24, the Company’s total borrowings consist of both short-term and long-term

debt, primarily utilized for working capital management and expansion purposes.

Repayments on the long-term loan under TERF are being made progressively over

time, secured against a pledge of fixed assets.

Total borrowings slightly decreased to PKR 2,682 million in FY24, compared to

PKR 2,705 million in FY23. The Company’s capital structure remains

well-balanced, with a solid equity base of PKR 2.7 billion in FY24. This growth

in equity strengthens the Company’s financial position, providing a buffer

against financial risks and reinforcing its capacity to service debt. Going

forward, the leverage ratio is expected to remain stable, as the Company has no

plans for additional long-term debt borrowing.

|