Profile

Legal Structure

Pakistan National Shipping Corporation (herein referred to as the "PNSC" or "the Corporation") is an autonomous corporation, functioning under the control of the Ministry of Maritime Affairs, Government of Pakistan. The Corporation is listed on the Pakistan Stock Exchange since 1980, and has nineteen subsidiaries and one associated concern.

Background

PNSC came into existence by the merger of National Shipping Corporation (NSC) and Pakistan Shipping Corporation (PSC) in 1979 through Pakistan National Shipping Corporation Ordinance, No XX, 1979. The Corporation is entirely autonomous and is managed by its Board of Directors (BoD).

Operations

PNSC, being the national flag carrier of Pakistan, is involved in the transportation of dry bulk and liquid cargoes globally through managed and chartered vessels. The Corporation manages a fleet of 12 vessels, consisting of 7 tankers and 5 bulk carriers. The cargo carrying capacity of PNSC stands at ~938,876 DWT as at End-Sep'24. A small portion of PNSC's operations also comprises income from real estate business.

Ownership

Ownership Structure

PNSC is majorly owned by the Government of Pakistan (GoP) (87.56%), through the Ministry of Maritime Affairs, followed by the PNSC Employees Empowerment Trust (1.57%), bringing the total GoP holding to 89.13%. As a listed company, the remaining shares are distributed among the general public and financial institutions.

Stability

The Corporation has a stable ownership structure, with the GoP holding majority shareholding since its inception, ensuring consistent oversight and strategic direction through the Ministry of Maritime Affairs. Additionally, the enactment of the State-Owned Enterprise (Governance and Operations) Act, 2023 (SOE Act), along with the issuance of the State-Owned Enterprise (Operation & Management) Policy (SOE Policy) in November 2023, further strengthens its governance framework. Under Section 9(a) of Chapter 3 of the SOE Policy, the Corporation has been classified as a Strategic SOE by the Cabinet Committee on State-Owned Enterprises.

Business Acumen

The Corporation was formed under constitutional protection with an objective of providing the Country with a national flag shipping service. Major stakeholder in the Corporation is the GoP, combined with the Corporation's experience in navigating complex global maritime markets and maintaining operational efficiency, reinforces its strong business acumen.

Financial Strength

The financial strength of the Corporation is considered strong due to the majority ownership of the GoP. The Corporation is a non-budgetary autonomous body utilizes its own resources.

Governance

Board Structure

The PNSC Board of Directors (BoD) currently comprises ten members, with eight directors appointed by the Federal Government, including two Ex-officio Directors and the Chairman. Additionally, two directors are elected by shareholders for a term of three years. The Chief Executive Officer will be appointed by the Federal Government from a pool of three candidates recommended by the Board.

Members’ Profile

The Federal Government, through its Cabinet decision, approved the appointment of five Directors to the PNSC Board for a three-year term starting September 23, 2024. These include Mr. Sultan A. Chawla the Chairman of the BoD, Mr. Arif Habib, Mr. Khalil Ahmed, Mr. Khawaja Shahzeb Akram, and Ms. Nadia Osman Jung. Other members are Mr. Qumar Sarwar Abbasi, Additional Finance Secretary (Corporate Finance); Mr. Umar Zafar Sheikh, Additional Secretary, Ministry of Maritime Affairs; Mr. Muhammad Ali, a seasoned energy and petrochemical expert currently leading JS Group’s industrial portfolio; Capt. Sarfaraz Inayatullah Qureshi, a reputed engineer and naval architect with over 41 years of maritime experience; and Mr. Ahsan Ali Malik, Group Director of The Waterlink Group with expertise in shipping, energy, and infrastructure development. This well-rounded Board brings diverse expertise and strong leadership to PNSC.

Board Effectiveness

The PNSC Board has established four committees to strengthen governance and oversight: (i) Audit Committee, chaired by Mr. Muhammad Ali, (ii) Procurement Committee, led by Mr. Khalil Ahmed, (iii) HR, Nomination, and CSR Committee, headed by Mr. Arif Habib, and (iv) Strategy and Risk Management Committee, chaired by Ms. Nadia Osman Jung. The frequency of meetings for the aforementioned committees is as follows: The Audit & Finance Committee held five quarterly meetings, while the HR, Nomination, and CSR Committee convened fifteen meetings on an as-needed basis. The Strategy and Risk Management Committee, along with the Vessels Procurement Committee, met as required, depending on specific needs and circumstances. The Corporation remains committed to good governance, aligning its practices with the Companies Act 2017, Pakistan Stock Exchange rules, and the Listed Companies (Code of Corporate Governance) Regulations, 2019.

Financial Transparency

The Corporation has an effective internal audit department, while GT Anjum Rehman Chartered Accountants and Yousuf Adil Chartered Accountants serve as the external auditors. They have provided an unqualified opinion and review on the consolidated financial statements for the year ended June 30th, 2024.

Management

Organizational Structure

PNSC has a well-defined organizational structure supported by a professional management team. The reporting lines are clearly established, ensuring efficient communication and accountability within the Corporation.

Management Team

Seasoned professionals with long-standing associations with PNSC hold key management positions within the Corporation. Rear Admiral Jawad Ahmed, SI (M), was relieved of his duties as CEO on March 3rd, 2024, and the position remains vacant, awaiting appointment by the Federal Government. The management team is strengthened by Mr. S. Jarar Haider Kazmi, Executive Director (Finance) / Chief Financial Officer of PNSC, who has been with the PNSC Group since October 2005 and has a 29-year career in finance. Mr. Khurram Mirza, Executive Director (Special Projects & Planning), is a Certified Management Accountant (CMA) from the Institute of Management Accountants (IMA), USA, and has been involved in numerous business development projects both domestically and internationally. Captain Mustafa Kizilbash, Executive Director (Commercial), is a Fellow Member of the Institute of Chartered Shipbrokers, UK., Mr. Syed Muhammad Babur, Executive Director (Ship Management), is an engineer with expertise in analyzing organizational needs and translating them into achievable goals through teamwork. Mr. Zeeshan Taqvi, Chief Accountant, is a Fellow Member of the Institute of Chartered Accountants of Pakistan (ICAP). Additionally, the team includes Mr. Muhammad Javid Ansari, Company Secretary, and Mr. Fayyaz Amin Malik, Chief Internal Auditor. All of these professionals are supported by an experienced team, ensuring the efficient operations and governance of the Corporation.

Effectiveness

To maintain effective oversight of business operations, twelve management committees have been established, comprising various key management personnel. These committees play a crucial role in ensuring efficient decision-making, strategic planning, and the overall smooth functioning of the Corporation.

MIS

PNSC employs the "DANAOS" Enterprise Resource Planning (ERP) software for its Management Information System (MIS) reporting, replacing the previously used "Ship Management Expert System" (SES). This system facilitates an online connection between the vessels and the head office, ensuring real-time data sharing and operational efficiency. Additionally, the Corporation utilizes "Purple Finder," an international satellite tracking system, to monitor its fleet. With equipment trackers installed on the vessels, this system enables accurate and continuous tracking of the fleet's location.

Control Environment

The Corporation relishes on strong governance practices and a well-structured management system. It features a hierarchical organizational structure with clearly defined lines of responsibility, ensuring accountability at all levels. This is further supported by an integrated, well-established information system that effectively supports the functions essential to a shipping corporation.

Business Risk

Industry Dynamics

The shipping industry is experiencing strong performance, with the Clark Sea Index averaging $24,000/day in Q1, 35% above the 10-year trend, continuing the positive momentum from 2023. Seaborne trade volumes rose by 3% in 2023 to 12.4 billion tons, with a projected 2% increase to 12.6 billion tons in 2024. Container markets saw a boost from Red Sea rerouting, doubling spot freight rates and increasing charter rates by 37% since December. Bulk carriers are off to a strong start with steady cargo volumes and limited new build orders. Fleet growth is projected at ~3%, reaching 2.5 billion dwt in 2024.

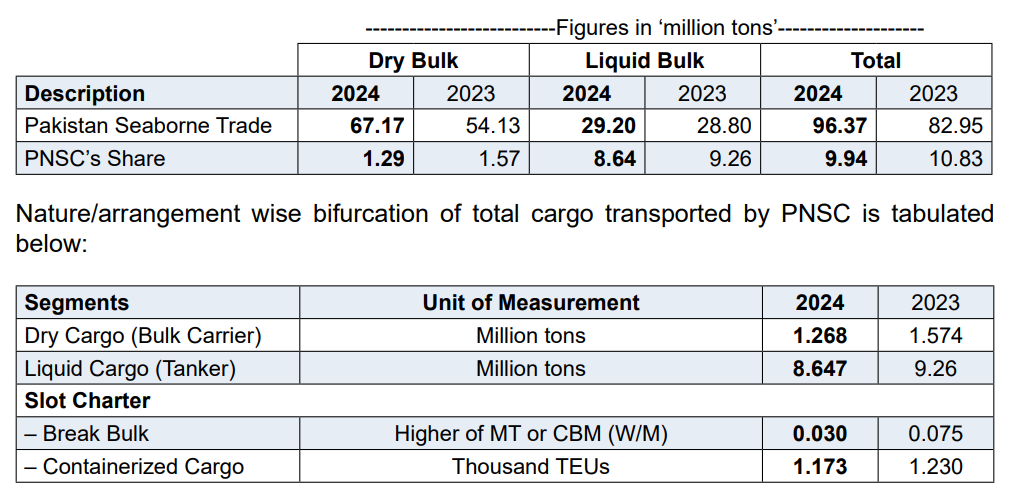

Relative Position

PNSC, with a total DWT capacity of 938,876 metric tons, transported approximately 9.94mln tons of cargo during FY24, (FY 2023: 10.83mln tons), accounting for about 10.31% (FY 2023: 13.06%) of the country's total seaborne trade volume of 96.37mln tons (FY 2023: 82.95mln tons). The liquid bulk segment primarily includes crude oil variants imported by refineries and OMCs, with white oil (e.g., MOGAS) gaining prominence due to a global and domestic shift toward cleaner energy sources. PNSC holds a significant ~32% share in liquid bulk cargo and ~2% in dry bulk. As the sole national flag carrier, PNSC operates a fleet of bulk carriers and oil tankers, representing 100% of Pakistan's registered fleet.

Revenues

During FY24, PNSC's revenue declined by 15% to PKR 46,363mln (FY23: PKR 54,597mln), with 1QFY25 turnover at PKR 10,839mln (1QFY24: PKR 13,296mln). Revenue from crude oil and charter-in vessels fell by PKR 835mln and PKR 1,880mln, respectively, while dry cargo revenue improved by 20% (PKR 210mln) due to higher charter rates. Key factors contributing to the decline in revenue included lower refinery freight rates ($11.39/MT vs. $12.44/MT), a drop in the World Scale index (6.17 vs. 6.77), and a 5% decline in the USD exchange rate (PKR 278 vs. PKR 293). However, bulk carrier charter rates increased by 28% year-on-year. The AFRA rate remained relatively stable at $169/MT in 1QFY25 but declined significantly from $214/MT in FY23, contributing to the lower revenue in FY24.

Margins

During FY24, the gross profit margin declined to approximately 41%, compared to ~50% in the same period last year (SPLY). This reduction was primarily driven by a 21% drop in average AFRA rates, from 214 to 169, and a 39% decrease in the average charter rate per day, from USD 13,894 to USD 8,504. Additionally, costs increased significantly due to the following factors:

• Higher depreciation expenses resulting from the capitalization of drydocking costs.

• A substantial rise in repair and maintenance expenses as well as stores and spares consumption, necessitated by extensive maintenance work required for the ageing fleet.

Consequently, net profit margins declined to 43% in FY24, compared to 55% in FY23.

In 1QFY25, gross and net margins improved, standing at 44% and 52%, respectively. The improvement in net margins was primarily due to:

• A 24% increase in other income, driven by efficient treasury management.

• A 65% reduction in group-level finance costs, resulting from the full repayment of a long-term loan for the procurement of two LR-1 vessels, M.T. Bolan and M.T. Khairpur, in September 2023.

Sustainability

PNSC’s fleet currently includes five aging Aframax tankers nearing the end of their operational life. In response to global pressures for fleet renewal and stricter decarbonization regulations set for 2030 and 2050, PNSC has launched a modernization strategy by tendering for up to four new Aframax/LR-2 tankers. This move aims to replace the aging fleet with environmentally compliant, future-ready vessels. Opting for new builds over secondhand tonnage underscores PNSC’s focus on sustainability, operational efficiency, and long-term competitiveness, while aligning with global trends in environmental responsibility.

Financial Risk

Working capital

During FY24, the Corporation's working capital requirements remained low, primarily supported by internal cash flow generation. The business model demonstrates a well-optimized cash conversion and payment cycle, reflected in its sound gross working capital days (14 days in FY24, improving to 11 days in 1QFY25) and net working capital days (10 days in FY24, reduced to 7 days in 1QFY25).

Coverages

During 1QFY25, the Corporation's financial performance showed significant improvement in cash flow and debt management. Free Cash Flow from Operations (FCFO) increased to 43.6x, up from 23.1x in FY24 and 20.7x in FY23, driven by periodic loan repayments leading to reduced borrowings. Additionally, the interest coverage ratio remained strong at 13.5x, indicating strong capacity to meet interest obligations and improved financial stability.

Capitalization

The Corporation maintains a low-leverage structure, with a debt-to-equity ratio of 2.7% in 1QFY25, slightly down from 3.1% in FY24, reflecting minimal long-term borrowings. However, the planned acquisition of new vessels will necessitate substantial capital investment, likely increasing gearing levels. This could moderate the Corporation's strong financial metrics in the future, requiring careful management to balance growth and financial stability.

|