Profile

Legal Structure

EXIDE Pakistan Limited (referred to as "EXIDE" or "the Company") is a public limited company incorporated in Pakistan in 1953. It was listed on the Karachi Stock Exchange (now the Pakistan Stock Exchange) in 1982. The Company's registered office is situated at A-44, Hill Street, Off Manghopir Road, S.I.T.E, Karachi.

Background

EXIDE was initially incorporated as a private limited company in partnership with Chloride Group PLC of the United Kingdom. At the time, Chloride Group PLC had a presence in 35 countries worldwide and provided technical support through its Chloride Technical division to help establish EXIDE's operations. Over the years, the Company has significantly expanded its production capacities and broadened its geographical reach. In 1991, EXIDE strengthened its position as a leading battery manufacturer in Pakistan by acquiring Furukawa Battery, an automotive battery company. To further diversify its product portfolio, EXIDE established a plant for the production of sulfuric acid and has also ventured into the solar power solutions market.

Operations

The Company's principal business operations include the manufacturing of batteries, chemicals, and acids. Its manufacturing facilities are located at S.I.T.E. Karachi and Hub, Balochistan, while the chemical and acid production units are based at S.I.T.E. and Bin Qasim, Karachi. In FY24, the battery plant operated at approximately 85% capacity utilization, while the chemical plant maintained a utilization rate of around 75%. Additionally, EXIDE has developed a nationwide dealer network for the distribution and sale of its batteries.

Ownership

Ownership Structure

The majority of EXIDE's shareholding is held by the sponsoring family, which collectively owns approximately 75.54% of the Company's shares. Financial institutions, including mutual funds, hold around 11.47%, while the remaining 12.99% is held by the general public.

Stability

The majority of the Company's shares are concentrated in the hands of the sponsoring family. There have been no significant changes in the ownership structure in recent years, and no such changes are expected in the foreseeable future. As a result, the ownership structure is considered stable.

Business Acumen

The sponsoring family has been at the helm of EXIDE since 1991, bringing over three decades of experience in the battery manufacturing industry. Mr. Altaf Hashwani, a key figure in the family, also serves as the managing partner of Sana Safina Fashion Resources. The enduring success of these ventures highlights the sponsors' significant business acumen and their ability to lead and grow diverse enterprises.

Financial Strength

As of March 2024, EXIDE reported a topline of PKR 25,668mln and an equity base of PKR 6,280mln. In addition to their leadership of EXIDE, the sponsors have also expanded into the textile retail sector with their brand "Sana Safinaz," further demonstrating their strong financial position. This diversified business portfolio provides the sponsors with the financial strength to support EXIDE, should the need arise.

Governance

Board Structure

The overall control of EXIDE rests with an eight-member Board of Directors, which includes four non-executive directors representing the sponsoring family, two executive directors (the CEO and CFO), and two independent directors. The Board's composition is further strengthened by the inclusion of two female directors, enhancing its diversity. Mr. Arif Hashwani serves as the Chairman of the Board.

Members’ Profile

Mr. Arif Hashwani has been serving as the chairman of the Company since 1991. He brings considerable experience in the related industry and has been instrumental in fostering growth and diversification of EXIDE. He is also the director/partner in other associated undertakings. Mr. Altaf Hashwani is a business graduate from the USA and has also completed the Directors’ training program from the Institute of Corporate Governance of Pakistan. He commanded the supply chain management of the Company and now serves as the CEO of SSFR (Pvt.) Ltd. The independent directors are well-regarded professionals and bring diverse expertise.

Board Effectiveness

The board has two committees in place to oversee and assist the Board in the company’s operational and financial matters. These committees include 1) the Audit Committee and 2) the Human Resource Committee. The board meetings are formally held with a pre-defined agenda. Minutes are diligently recorded and action points are communicated to the relevant stakeholders. During FY24, four meetings of the Board were conducted where the attendance of the directors remained strong.

Financial Transparency

The external auditors of the Company, Yousuf Adil & Co., are listed in the “A” category on the SBP’s panel of auditors. They issued an unqualified opinion on the Company’s financial statements for the year ended March 2024, indicating the Company's compliance with applicable policies and accounting principles.

Management

Organizational Structure

EXIDE has a well-defined organizational structure, comprising multiple functional departments, including Accounts and Finance, Marketing and Sales, Industrial, Corporate Sales, Production, Supply Chain, Information Technology, Human Resources, and Internal Audit. Each department is organized with a multilayered hierarchy, led by a qualified Head of Department. At present, all key positions within the organization are filled.

Management Team

Mr. Arshad Shahzada serves as the CEO of EXIDE, leading the management team. A graduate in Electrical Engineering from the University of Engineering and Technology, Lahore, he has been with the Company for over three decades and plays an active role in strategic business decisions and financial management. Before joining EXIDE, Mr. Shahzada gained experience in the sugar, petrochemical, and fertilizer industries. He is supported by a team of seasoned professionals, including Mr. S. Haider Mehdi, FCMA, the CFO, who has more than 40 years of experience and has been with EXIDE for 30 years. The management team is highly skilled with deep technical expertise and a long-standing association with the Company.

Effectiveness

A well-structured organizational framework with clearly defined responsibilities and reporting lines enhances the effectiveness of management. However, the establishment of management committees could further strengthen this by bridging inter-departmental gaps, fostering better collaboration, and enabling more efficient decision-making across operations.

MIS

EXIDE's core operating software is "SAP Enterprise ECC 6.0 EHP 5," which has been implemented at both the head office and all manufacturing sites. The system incorporates various modules, including Sales & Distribution, Materials Management, Production Planning, Financials, Controlling, and Human Resource Management. This comprehensive integration enables the Company to maintain a robust, real-time monitoring and reporting system, enhancing operational efficiency and decision-making.

Control Environment

The Company utilizes state-of-the-art technology in the production of batteries, chemicals, and acids, ensuring that its processes and products comply with both local and international quality standards. Additionally, EXIDE has a dedicated in-house internal audit department that plays a crucial role in identifying and assessing risks associated with the Company’s operations. The internal audit team also ensures the effective implementation of policies and standard operating procedures at all levels within the organization.

Business Risk

Industry Dynamics

Sales of batteries are closely linked to the severity of the energy crisis and the growth of the automobile sector in Pakistan. Currently, the organized battery market in the country is dominated by three key players: EXIDE, Atlas Battery Limited (AGS), and Pakistan Accumulators (Pvt.) Limited (Volta & Osaka). In recent years, Original Equipment Manufacturers (OEMs) in the automobile sector have experienced a significant decline in sales. However, the battery industry has remained relatively stable, primarily driven by strong demand from the replacement market. Additionally, the widespread adoption of solar power solutions, driven by load shedding and high energy tariffs, has further supported battery sales. Stable lead prices and a reduction in interest rates have also contributed to the industry's improved profitability and stability.

Relative Position

EXIDE is one of the leading players in Pakistan's battery industry, with a long-standing presence and strong market reputation. The Company has established warehouses in all major cities across the country and boasts a nationwide dealer network, which has significantly contributed to its growing market presence. Currently, EXIDE holds an estimated market share of approximately 18%, according to the management's representation.

Revenues

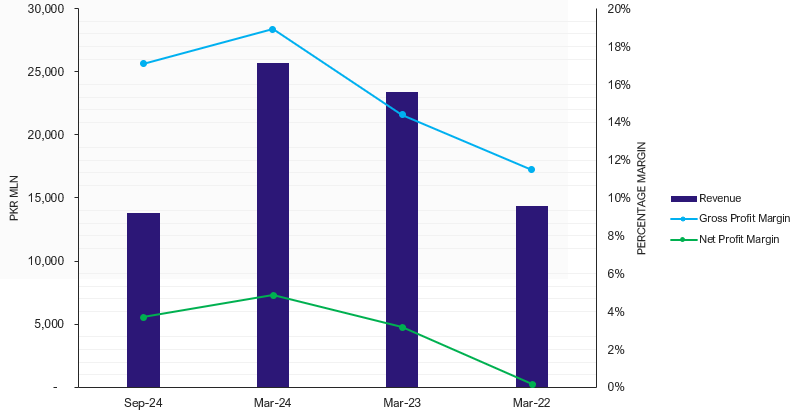

For the year ended March 2024 (FY24), EXIDE recorded a revenue of PKR 25,668mln, compared to PKR 23,402mln in March 2023, reflecting a year-on-year growth of ~9.7%. This growth was primarily driven by a surge in battery prices, aimed at offsetting the impact of increased production costs, although the volumes experienced a slight decline. Additionally, during the first half of FY25, the Company continued its growth trajectory, with an annualized topline growth of ~7.7%, primarily driven by increased volumetric offtake.

Chart-1: Revenue & Margins

Margins

EXIDE’s profit margins improved in FY24 compared to the previous year, largely driven by higher prices. As of March 2024, the Company's Gross Profit Margin stood at 18.9%, up from 14.4% in March 2023, while the Net Profit Margin increased to 4.9%, up from 3.2% in the previous year. These improvements were primarily due to price adjustments aimed at offsetting elevated production costs. The Company recorded a Profit After Tax of PKR 1,255mln for FY24, compared to PKR 755mln in March 2023. However, during the first half of FY25, the Company’s margins were slightly diluted due to rising energy costs and increased taxation, which could not be fully passed on to customers because of intense industry competition.

Sustainability

EXIDE is actively pursuing growth strategies focused on both market and product penetration. The Company is expanding its customer base and exploring new areas for sales growth. In line with evolving market trends, EXIDE has also diversified its product portfolio by introducing new types of batteries, such as tubular and maintenance-free batteries, to meet changing customer demands. Additionally, the management remains proactive in assessing future earnings potential, continuously evaluating performance through budgets and financial projections to ensure sustained growth and profitability.

Financial Risk

Working capital

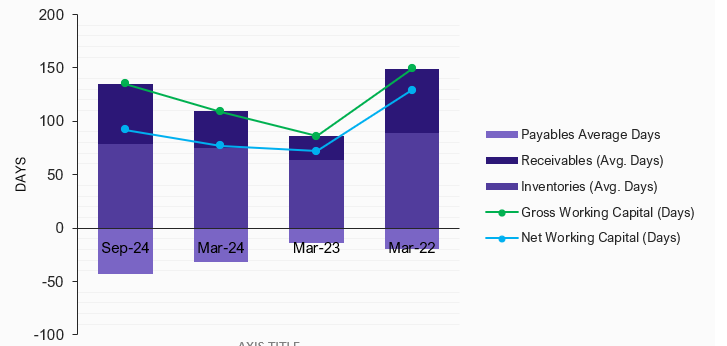

The Company relied on internally generated cashflows and short-term borrowings for its working capital management. The Company's cash cycle has stretched during FY24 compared to the year ended March 2023, as the net working capital days of the Company stood at 78 days (March 23: 72 days) mainly on the back of the pile of inventory in anticipation of peak demand. Furthermore, the Company’s net working capital cycle further stretched to ~92 days during 6MFY25 owing to an increase in receivables days triggered by increased credit time allowed by the Company to incentivize dealers as a strategy to combat intense competition.

Chart-2: Working Capital

Coverages

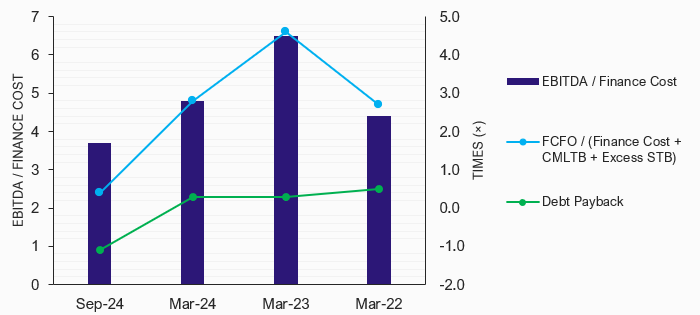

During FY24, the Company’s coverages diluted compared to last year owing to an increase in borrowings and finance costs of the Company. EXIDE’s interest coverage was recorded at 2.9x compared to 4.9x in FY23. However, the debt payback period remained static at 0.3 years. During 6MFY25, a decrease in EBITDA further diluted the coverages of the Company as reflected by an interest coverage ratio of 0.4x.

Chart-3: Coverages

Capitalization

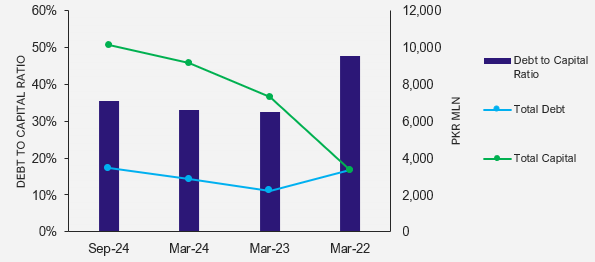

At the end of Sep-24, total borrowing of the Company stood at PKR 3,436mln out of which PKR 3,229mln consisted of short-term borrowings. The Company has availed credit lines from various financial institutions including Meezan Bank Limited and Bank-Alfalah Limited. The seasonal sales cycle of the Company has resulted in increased leverage as the Company needs investment in working capital to boost production in winter in anticipation of peak demand in summer.

Chart-4: Capitalization

|