Profile

Legal Structure

Denim-E (Private) Limited ("Denim-E" or "the Company") was incorporated on August 13, 2018, as a Private Limited Company.

Background

Denim-E (Private) Limited is a family-owned private limited company. The sponsoring family has been involved in diverse ventures such as real estate, and biogas business. In 2018, the family set its footprint in the textile sector by establishing Denim-E. The Company specializes in exporting fashion apparel, with a focus on denim jeans, to international markets.

Operations

The Company is principally engaged in the manufacturing and export of denim and knitted garments. The Company has cut

to pack capacity of 15,000 Pieces/day which accumulates to 450,000 per month and 5.4mln Pieces annually. The Company’s total energy requirement is 600 kw.

The requirement is met through various captive sources (Coal, Gas, Furnace Oil), WAPDA, etc, and in housed deployed Solar Panel as well. The registered office of the Company is

situated at Plot 100, and 19 Sector 27 Korangi Industrial Area, Karachi.

Ownership

Ownership Structure

The ownership of the Company rests with Mr. Azhar Khalid and his wife. following the passing of Mr. Khalid Farooq, his ownership stake was transferred to his son, Mr. Azhar. Additionally, Mr. Rizwan Raza has formally exited the company, resulting in a change to the ownership structure. The major shareholding of the

Company is owned by Mr. Azhar Khalid (~95%), while Mrs Laila holds a ~5% stake in the Company.

Stability

Mr. Azhar Khalid, the founder and principal shareholder of the Company, holds a dominant 95% ownership stake, ensuring a high degree of stability in the Company's ownership structure. However, there is no formal succession planning in place and its establishment will augment the ownership profile of the Company.

Business Acumen

Mr. Azhar Khalid, a BSc (Hons.) graduate from the Textile Institute of Pakistan (TIP), possesses over a decade of experience in the textile industry. Through years of hands-on involvement, he has developed deep expertise and strategic business acumen, equipping him to navigate and sustain the Company through any forthcoming challenges. Known for his persistence and ability to see tasks through to completion, he is regarded as man of the last mile.

Financial Strength

Denim-E is the sole business venture of the sponsor. In the event of a financial crunch, funding is expected to be sourced either from internally generated cash flows or through external debt, leveraging the sponsor's financial strength. The financial strength of the Company is considered adequate.

Governance

Board Structure

The Company has a two-member board with the presence of sponsors and their families. The position of CEO is vested with Mr M. Azhar Khalid. Ms. Laila, wife of Mr. Azhar serves the board in the capacity of director. The inclusion of independent oversight will improve the governance framework of the Company.

Members’ Profile

Mr. Azhar, the founder and CEO of Denim-E (Pvt.) Ltd brings strong business acumen and industry expertise, backed by a BSC (Hons) from the Textile Institute of Pakistan (TIP). Before establishing his own venture, he gained valuable experience in marketing leadership and product development at top textile firms. His deep understanding of market dynamics, consumer trends, and supply chain operations has been instrumental in driving Denim-E’s growth and success.

Board Effectiveness

BoD meetings are held regularly in which discussion on various aspects is recorded in minutes and decision or actions are referred to the CEO. However, there are no board committees in place to assist the board and formation will augment the governance framework of the Company.

Financial Transparency

Grant Thornton Anjum Rahman Chartered Accountants, who are in category ‘A’ of SBP and have a QCR rating by ICAP, are the external

auditors of the company. They have expressed unqualified opinion on the financial statements of the company for the year ended June 30th, 2024.

Management

Organizational Structure

The organizational structure of the company is divided into eight functional departments, namely: (i) Production, (ii) Marketing, (iii) Admin,

Information Technology, Utilities & Maintenance, (iv) Finance & Audit, (v) HR & Compliance, (vi) Import/Export & Logistics, (vii) Procurement and (viii) Quality

external. The overall organizational structure is considered lean as all HODs report directly to the CEO.

Management Team

Mr.

Azhar has

fifteen years of professional experience and holds a BSC (Hons) from the

Textile Institute of Pakistan (TIP). Before founding Denim-E (Pvt.) Ltd, he has

experience six years in Rajby Industries as a head of marketing.

He has worked as a merchandiser and product developer at top textile houses of the Country.

Effectiveness

The management meetings are held periodically with follow-up points to resolve or proactively address operational issues, if any, eventually ensuring a

smooth flow of operations. Four management committees are in place to assist the management teams; namely, Workers Management Committee (to promote the development of social and stable labor-management relations), Environmental Health & Safety Committee ( to enhance and develop the safety policies and procedures for the workplace), Audit Committee ( to review financial and compliance risk), and Remuneration & Human Resource Committee (reviews compensation and reward policies.)

MIS

The company has implemented Odoo ERP as its Management Information System (MIS) to enhance efficiency, data accuracy, and decision-making. This integration centralizes key business functions, automates workflows, and provides real-time reports, reducing errors and improving productivity.

Control Environment

Denim-E utilizes management systems as their mechanism for ensuring control. There is clear evidence of these systems being audited and certified

externally. Examples of this include RCS (Recycled Claim Standard), BSCI, GOTS, OekoTex, GRS, WRAP, C-TPAT & OCS certifications. The internal audit department is in-house and is reportable to the Company's head of finance. The role of Internal Audit is to evaluate risk management, governance, and control processes as well as ensuring the adequacy of existing internal controls.

Business Risk

Industry Dynamics

The textile exports of the country reached USD 16.7bln in FY24, a slight increase from USD 16.5bln in the previous year, reflecting a growth of 0.93% YoY. The highest contribution came from the composite and garments segment at USD 9.1bln, followed by the weaving segment at USD 6.5bln and the spinning segment at USD 1.0bln. During 5MFY25, the textile exports stood at USD 7.6bln. In FY25, the transition from the final tax regime to the normal tax regime is set to impact the profitability matrix of export-oriented units, with a 29% tax on profits and a super tax of up to 10%. The consistent decline in policy rates over the last two quarters, along with the anticipation of further reductions, is expected to provide a cushion in the financial metrics of the industry

Relative Position

Denim-E was formed with one vision in mind and that was

to be the first denim manufacturing Company in Pakistan to be fully sustainable from its very inception. The Company operates with 1,026 stitching machines, reflecting its adequate presence in the country's textile sector. The Company is relatively new in the market and operates as a low-tier player in the dedicated denim segment. The Company’s plan of enhancing current capacity will assist in

strengthening its footprint, going forward

Revenues

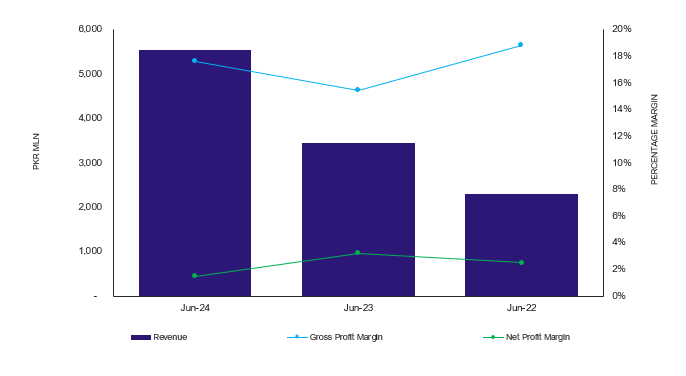

An analysis of the past three years indicates substantial revenue growth for the company. In FY24, the company's topline exhibited a significant improvement, reaching PKR 5,550 million, up from PKR 3,457 million in FY23—representing a remarkable 60% surge. The company's sales are predominantly concentrated in international markets, particularly in the European region. This upward trend is primarily driven by an increase in sales volume by the existing clients. The Company is mindful of expanding its customer base in the future and expanding business in different regions. In Sep'24, the Company's top line stood at PKR 1.5bln.

Margins

During FY24, the Company’s gross profits increased to PKR 979mln (FY23: PKR 532mln), attributable to volumetric growth. Consequently, the gross profit margin stood at 17.6%

(FY23: 15.4%). Administrative and general expenses, along with selling and distribution expenses recorded an increase largely in line with inflationary pressure. Thus, the operating margin also inclined to 2.9% (FY23: 1.1%). Finance cost declined to PKR 83mln (FY23: PKR 122mln) Hence, the net profitability clocked in at PKR 81mln (FY23:

PKR 112mln). The net profit margin reflected a decrease and clocked at 1.5% (FY23:

3.2%) due to the higher tax burden due to the transition from FTR to NTR for export-oriented units.

Sustainability

The Company

has demonstrated volumetric growth in the last three years despite the

inflationary pressure, and prolonged high interest rates. The Company has sold

3.1mln pieces during FY24 (FY23: 2.1mln pieces). As per the management

discussion, the Company is on its course to surpass 4 million pieces in sales

during FY25. Based on financial projections, it is anticipated that the Company will enter into the top 100 textile exporters list of the country. It is expected that the Company will look to expand its customer base by acquiring USA-based clients going forward.

Financial Risk

Working capital

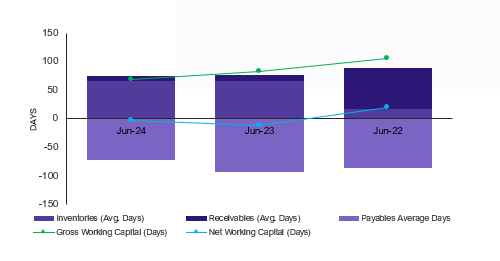

During FY24, the Company’s gross working capital cycle recorded a sizable decline to 69 days (FY23: 82 days) attributable to the attrition in

receivable days (FY24: 3 days, FY23: 16 days). The Company’s net trade assets increased and clocked at PKR 1,458mln (FY23: PKR 1,040mln). The current ratio of the Company stood at 0.8x (FY23: 0.9x).

Coverages

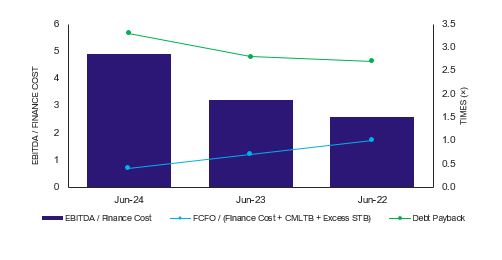

The Company's Free Cash Flows from Operations (FCFO) marginally decreased in FY24 and clocked in at PKR 312mln(FY23: PKR 318mln). The interest coverage ratio inclined to 4.1x in FY24 from 2.8x in FY23 attributable to the sizable decline in the finance cost. The debt coverage was recorded at 0.4x (FY23: 0.7x).

Capitalization

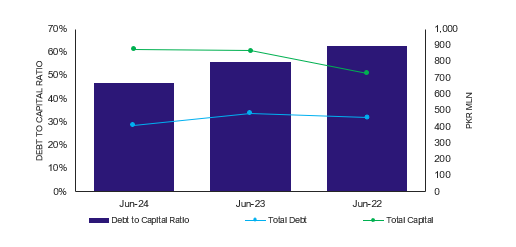

Denim-E is moderately leveraged at (~46.9%) in FY24 this ratio has declined for the past 3 years (FY23: ~55.8%, FY22: ~62.8%), driven by the retention of accumulated profits, which continues to enhance its equity base. The Company’s total borrowings clocked at PKR 411mln, (FY23: PKR 482mln). The decline is attributable to a decrease in the long-term borrowings. The Company's short-term borrowings clocked at PKR 223mln (FY23: 208mln), which constitute ~54.2% of the total borrowings. The Company’s equity base witnessed a YoY incline to PKR 466mln (FY23: PKR 385mln).

|