Profile

Legal Structure

US Denim Mills (Private). Limited ("UDML" or "the Company") was incorporated on January 18, 2005, as a private Company.

Background

The Company is categorized under the fabric vertical of the US Group. The group established its first manufacturing facility in 1985, and over the years, it strategically expanded its business operations in the textile sector, emerging as a prominent business group. With evolving industry trends, the group shifted its focus to denim jeans in 2008.

Operations

The Company is engaged in the manufacturing and sale of denim fabric. Its registered office and manufacturing facility are located at 3-KM, Defence Raiwind Road, Lahore. UDML has a wholly-owned subsidiary, US Fashion Turkey Tekstil Ticaret Anonim Sirketi. The Company’s manufacturing facility is equipped with 229 air-jet looms and 20 power looms. The total energy requirement of the Company is 596,479 mmBTU, primarily met through natural gas and biomass as the main energy sources. However, secondary sources, including diesel, furnace oil, WAPDA, LPG, and solar power, are on standby to ensure continuity in case of the unavailability of the primary sources.

Ownership

Ownership Structure

UDML is a prominent business venture of two sponsoring families (Mr. Mian Muhammad Ahsan & Mr. Javed Arshad Bhatti) of the US (Umer-Siddique) Group. It is a wholly owned subsidiary of AJ Holdings (Private) Limited. The holding Company exercises its control over the Company’s

board by virtue of its 100% stake in the Company.

Stability

The entire ownership is held by the sponsoring group, which primarily oversees investments in subsidiary and associated companies, ensuring the stability of the corporate structure. So, the Company's ownership structure is expected to remain stable in the foreseeable future.

Business Acumen

US Group is recognized as the leading exporter of denim and twill in Pakistan, supported by a rich history of operations in the textile industry. Despite its focus on a

single sector, the group has consistently demonstrated resilience and growth through various economic cycles.

Financial Strength

The Company’s affiliation with the US group demonstrates the strong financial muscle of the sponsors. According to the US Group Sustainability

Report CY23, the group size is estimated at USD 356mln. The group includes four additional companies within the industry: (i) US Apparel & Textiles (Pvt). Limited, (ii) Stylers International Limited,

(iii) US Workwear and (iv) US Dyeing & Finishing. The sponsors have a strong capacity to support the Company if needed.

Governance

Board Structure

The overall control of the board rests with ten members from the sponsoring families.

Members’ Profile

The two founders of the U.S Group, Mr. Javed Arshad Bhatti, Chairman of the Board, and Mr. Mian Muhammad Ahsan, have been associated with the Company for over 18 years. All board members have relevant stature and extensive experience, which bodes well for the consistent growth and long-term sustainability of the Company.

Board Effectiveness

The Company has established two committees to oversee key business matters: the Audit Committee and the Performance Assessment Committee. Board meetings are held monthly to review operations and assess the progress toward targets. The discussions on various aspects are formally documented in meeting minutes; however, there is still room for improvement.

Financial Transparency

To uphold high standards of transparency, BDO Ebrahim & Co. Chartered Accountants have been appointed as the external auditors

of the Company rated in "Category A" by the SBP panel of auditors. They expressed an unqualified opinion on the financial statements of the Company for the year ended June 30th, 2024.

Management

Organizational Structure

The Company maintains a well-defined organizational structure divided into several functional departments, namely: (i) Finance, (ii) Marketing, (iii) Quality

Assurance, (iv) Operations, (v) Information Technology, (vi) Supply Chain, and (vii) HR & Admin, and procurement functions. All departments report to their respective

GM(s), who are responsible for delivering the bottom line and achieving targets. All the GMs report to the CEO.

Management Team

Mr. Irfan Nazir Ahmad, the CEO, holds an MBA qualification and boasts 26 years of ample experience in the Textile & Apparel Industry, covering

Sales & Marketing, General Management, Production Management, and Supply Chain. His tenure includes roles at Reshi Textiles, Azgard 9 Limited, US Denim, and US

Apparel, followed by an association with the US group since 2014. Mr. Syed Farrukh Ali, the CFO, has been associated with the group since 2001. He is a Chartered Management

Accountant.

Effectiveness

The Company has established two formal management committees: the Purchase Committee and the Waste Management Committee. Regular management meetings are held to discuss and address operational issues, with follow-up actions taken to resolve any challenges proactively. These meetings are led by the Company's CEO.

MIS

The Company’s daily and monthly Management Information System (MIS) includes comprehensive performance reports, which are regularly reviewed by senior management. Acknowledging the importance of robust information systems to ensure operational efficiency, the Company has implemented the Oracle-based ERP solution, Oracle E-Business Suite, Harmony version 4, to streamline processes and enhance decision-making capabilities.

Control Environment

US Denim utilizes management systems as its mechanism for ensuring effective controls. There is clear evidence of these systems being audited and certified

externally. Examples of this include ISO 14001, GOTS, C2C at the gold level, AWS, OCS, GRS, RCS, Higg FEM 3.0, SLCP, ICS Environment, BSCI, and Oeko-Tex.

Business Risk

Industry Dynamics

The textile exports of the country reached USD 16.7bln in FY24, a slight increase from USD 16.5bln in the previous year, reflecting a growth of 0.93% YoY. The highest contribution came from the composite and garments segment at USD 9.1bln, followed by the weaving segment at USD 6.5bln and the spinning segment at USD 1.0bln. During 6MFY25, the textile exports stood at USD 9.1bln. In FY25, the transition from the final tax regime to the normal tax regime is set to impact the profitability matrix of export-oriented units, with a 29% tax on profits and a super tax of up to 10%. The consistent decline in policy rates over the last two quarters, along with the anticipation of further reductions, is expected to provide a cushion in the financial metrics of the industry.

Relative Position

US Denim Mills (Private) Limited is recognized as one of the top 100 textile exporters in Pakistan for FY24, positioning the Company in the mid-tier of the industry.

Revenues

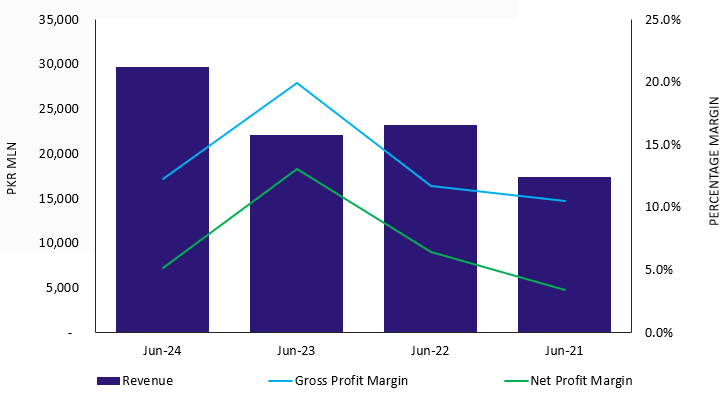

The Company's topline CAGR witnessed a remarkable growth, indicating a 3-year CAGR of 34.6% from June 2022 to June 2024. A dominant portion of the Company's revenue base is derived from exports. During FY24, the Company's

topline experienced an upswing at PKR 29.6bln (FY23: PKR 22.0bln),

up by 34.5%, primarily driven by a surge in the business volumes. Indirect sales make up around 64.8% of the total revenue, contributing PKR 19.2bln (FY23: PKR 15.0bln). Due to a strategic change, the Company increased its direct exports to PKR 9.7bln (FY23: PKR 6.6bln), recording a growth of 47.0% on a

year-on-year basis. The Company’s diversified revenue concentration indicates a low geographic

concentration risk. Egypt is the prime export destination of the Company,

with a contribution of PKR 2.2bln, which accounts for 7.4%, followed by Bangladesh,

Turkiye, Sri Lanka, Uzbekistan, and a few others. Client concentration remained elevated due to the predominance of inter-group sales, however, the group's longstanding track record provides comfort. The local sales stood at PKR 716.6mln (FY23: PKR 386.9mln),

attributed to rising demand and consumption trends for denim products. Locally, the

Company mostly sells to several big players like Interloop Limited, Rajby Industries, and Artistic Apparels (Pvt). Limited, etc.

Margins

During FY24, the Company's gross profit

margin experienced a dip (FY24: 12.2%, FY23: 19.9%) primarily due to a modest reduction in product pricing and increased discounting availed by international customers. The operating margin stood at 7.8% (FY23: 15.1%),

followed by an increase in operating expenses, concomitant with inflationary trends. In FY24, the finance

cost was reported at PKR 52mln (FY23: PKR 36mln) as the Company majorly relies

on the interest-free loans from related parties. As a result, the Company’s bottom line

tumbled to PKR 1.5bln (FY23: PKR 2.8bln). The Company’s net profit went down to 5.1% in FY24 compared to 13.0% during the same corresponding period.

Sustainability

The management is cognizant of the energy cost risk and has taken proactive measures to mitigate its impact. To reduce dependency on conventional energy sources, the Company has successfully installed a ~1.9 megawatt solar, which is now fully operational. Looking ahead, the management plans to explore new export avenues and strategically increase the focus on direct export sales to strengthen the long-term sustainability profile.

Financial Risk

Working capital

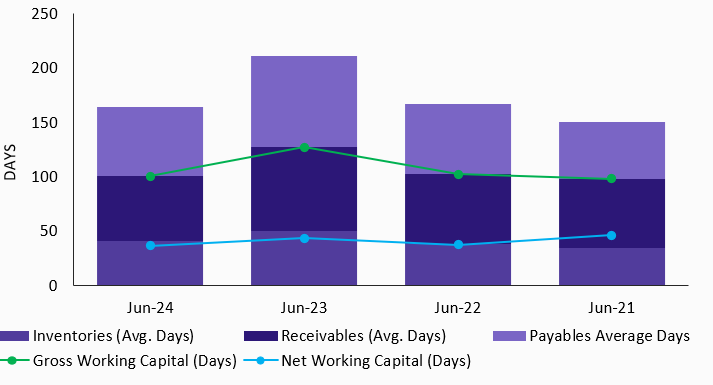

The Company's working capital cycle is driven by inventory days and trade receivable days, with the Company relying on internally generated cash flows and sponsor loans to effectively manage its operations. This approach allows the Company to maintain liquidity while minimizing reliance on external financing. As of end-Jun24, the Company's net working

capital cycle reflected improvement at 36 days (end-Jun23: 43 days) followed by optimization of the inventory cycle at 41 days

(end-Jun23: 50 days). The Company holds an ample borrowing capacity, as evidenced by the short-term trade leverage of 38.9% (end-Jun23: 41.5%).

Coverages

As of end-Jun24, the free cash flows from operations (FCFO) stood at PKR 1.8bln (end-Jun23: PKR 3.3bln), indicating adequate financial management. Despite this decrease, the Company's interest coverage and

core operating coverage remained in a comfortable range. However, the increase in total borrowings led to a rise in the Company's debt payback period clocking at 0.8 years (end-Jun23: 0.2

years).

Capitalization

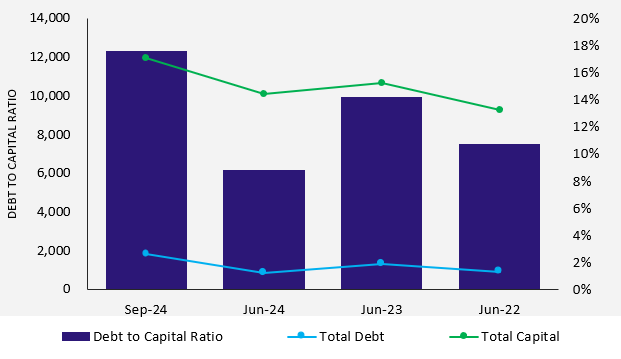

The

Company has maintained a low-leveraged capital structure. The sponsors have a

conservative approach towards interest-bearing loans; therefore, the Company’s

debt profile majorly comprises interest-free loans, followed by a minute contribution from

the SBP's subsidized facility (Export Financing Scheme). As of end-Jun24, the total leveraging illustrated an upward trend and clocked at 17.6% (end-Jun23: 8.8%), attributed to a rise in related party exposure to meet the extensive working capital requirments. The Company's equity base clocked at PKR

8.3bln (end-Jun23: PKR 8.4bln).

|