Profile

Legal Structure

Mount Fuji Textile Limited (‘Mount Fuji’ or ‘The Company’) is a Public (unlisted) Limited Company. It was incorporated in Karachi, Pakistan on

August 12, 1986.

Background

Over the years, Mount Fuji has steadily expanded its operations, diversifying its expertise across multiple stages of the manufacturing process. With a strong foundation in production excellence, the company has continuously evolved to meet market demands. As part of its growth strategy, Mount Fuji has successfully ventured into the garments segment, further strengthening its presence in the industry and broadening its portfolio of high-quality products.

Operations

The principal activity of the Company is the manufacturing and export of garments and home textile products. The company has three units. The Company

has five sectional warping machines of 1000 creels each with a warping capacity of approximately Two Million Meters a month. The Company has also a weaving facility

of 138 Sulzer and 84 Airjet Looms with a weaving capacity of approximately 3.5mln Picks a day. The Company has 15 knitting machines, 2 raising machines, 846

computerized sewing machines & 19 cutting machines. The energy requirement of the Company stands at 1.5 MW, primarily met through solar capacity and K-electric. The registered office is located at D-148 Sindh Industrial Estate (S.I.T.E) Karachi.

Ownership

Ownership Structure

The ownership of the Company rests with the family of Mr. Ashraf including his sons. The major shareholding of the Company is owned by Mr.

Ahmed Ashraf (28.57%), while the remaining is equally distributed between the sons, Mr. Abdul Latif Ashraf, Mr. Muhammad Ashraf, and Mr. Shehzad Ashraf.

Stability

The Company was established to facilitate the transfer of technical and business expertise from the first generation to the second generation of the Ashraf family. It integrates the experience and guidance of the founding generation with the leadership of the next generation. While a formal succession plan has not yet been announced, the establishment of the formal family constitution will augment the ownership profile of the Company.

Business Acumen

The Company's directors and management possess extensive expertise and a wealth of experience in the textile industry, having successfully led the organization for 38 years. Committed to its core philosophy, the Company strives for sustainable growth while upholding operational excellence and adhering to industry best practices.

Financial Strength

The sponsoring family has been involved in multiple businesses for more than 20 years. The family is involved in textile & garment manufacturing.

This indicates sponsors’ ability to provide support if the need arises.

Governance

Board Structure

Mount Fuji’s board comprises four members, including the Chairman - Mr. Ahmed Ashraf, and the Chief Executive Officer (CEO) – Mr. Abdul Latif

Ashraf. There are no independent directors on the board. The Company’s board is dominated by sponsor-family members and lacks independent oversight. The inclusion of independent oversight will enhance the governance profile of the Company.

Members’ Profile

Mr. Ahmed Ashraf, the Chairman of the Company, is a distinguished leader in the textile industry with over five decades of extensive experience. His journey in the sector began in the 1960s when he established Ashraf Trading Corporation, earning a reputation for reliability in textile exports. In 1986, he further demonstrated his strategic vision by founding Mount Fuji Textiles Limited, reinforcing his commitment to industry excellence and growth.

Board Effectiveness

No formal board committees have been established by the Company. BoD meetings are held regularly in which discussion on various aspects is recorded in minutes and decisions or actions are referred to the CEO, Mr.

Abdul Latif Ashraf. The establishment of sub-committees will augment the board's effectiveness.

Financial Transparency

BDO Ebrahim & Co, Chartered Accountants, is the external auditor of the Company. The auditor has expressed an unqualified opinion on the

financial reports for the year ending 30th June 2024. The auditors fall under the category' A' of SBP’s panel of auditors.

Management

Organizational Structure

Mount Fuji Textiles Limited follows a hierarchical structure with the Chairman at the top, followed by the CEO, Managing Director, and COO, ensuring centralized decision-making. The company is functionally divided into Marketing & Operations, Production, Weaving, and Hub Management, each led by a General Manager for specialized efficiency. Financial oversight is managed by the CFO, with key roles in Accounts, Treasury, Inventory Management, and Internal Audit, ensuring governance and risk control. A dedicated Procurement, Admin/HR, and Compliance function enhances regulatory adherence and resource management. The presence of Export and Import Managers indicates a focus on international trade. This structure fosters operational efficiency, clear responsibilities, and seamless coordination, making it well-suited for a large manufacturing enterprise.

Management Team

Mr. Abdul Latif Ashraf – CEO – holds a Master’s degree and has been in the Textile business for the last two decades. He has been associated with the Company since 2001. Mr. Muhammad Ashraf – the managing director – holds a Master’s Degree from Karachi. He has been in the Textile

Business for the last one and a half decades. He looks after all types of Procurement & Marketing and has been associated with the Company since 2007. Mr. Shehzad Ashraf – the executive director – holds a Master’s

Degree from the U.K. He is looking at the Finance and Admin department. He has been in the Textile Business for the last five years.

Effectiveness

Mount Fujii does not have established formal management committees. However, various reports pertaining to the Company's sales and inventory movements, as well as purchases and procurement activities, are prepared and submitted to senior management as required.

MIS

The Company has built an in-house ERP to cater to its business needs. The senior management monitors the business performance through certain Key MIS reports.

Control Environment

Production is completely order driven, there is a rigorous quality check done on the end product by the QC department. The Company has obtained

ISO 9001, ISO 14001, GSV, BICI, OEKO-TEX, WCA, Sedex, & & SQP certifications.

Business Risk

Industry Dynamics

The textile exports

of the country reached USD 16.7bln in FY24, a slight increase from USD 16.5bln

in the previous year, reflecting a growth of 0.93% YoY. The highest

contribution came from the composite and garments segment at USD 9.1bln,

followed by the weaving segment at USD 6.5bln and the spinning segment at USD

1.0bln. During 6MFY25, the textile exports stood at USD 9.1bln. In FY25, the

transition from the final tax regime to the normal tax regime is set to impact

the profitability matrix of export-oriented units, with a 29% tax on profits

and a super tax of up to 10%. The consistent decline in policy rates over the

last two quarters, along with the anticipation of further reductions, is

expected to provide a cushion in the financial metrics of the industry

Relative Position

The Company has five sectional warping machines

of 1000 creels each with a warping capacity of approximately two million

meters a month. The company has also a weaving facility of 138 Sulzer and 84 air jet

looms with weaving capacity of approximately 3.5 million picks a day. The

Company has 15 knitting machines, 2 raising machines, 846 computerized sewing

machines & 19 cutting machines. Considering this, the relative position of

the Company is considered a low to mid-tier textile player in the overall textile sector.

Revenues

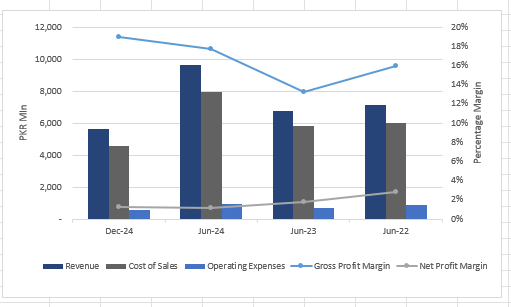

During FY24, the Company's revenue experienced a

year-on-year (YoY) growth of 43%, reaching PKR 9.6 bln(FY23: PKR 6.7bln). This growth was primarily driven by an increase in sales volume and

favorable pricing dynamics. A significant portion of the revenue is generated

from export sales, which stood at PKR 8.1bln (FY23: PKR 5.7bln). The

Company’s key export destinations include the UK, Poland, Spain, Germany, and

the USA. The Company boasts a diversified product portfolio, offering home

textile products (such as curtains, bedsheets, and comforters) as well as woven

and knitted garments. Among these, garments contribute the highest share to the

topline, generating PKR 3.6bln (FY23: PKR 2.5bln), followed by

bedsheets, which recorded PKR 2.9bln (FY23: PKR 2.1bln) in revenue. Meanwhile,

local sales saw a modest increase, reaching PKR 1.6bln (FY23: PKR 1.2bln) in FY24. During 1HFY25, the Company’s topline clocked at PKR 5.7bln (1HFY24:

PKR 5.6bln).

Margins

During FY24, the Company’s

gross profit witnessed a sizable incline (FY24: PKR 1.7bln, FY23: PKR 886mln) Consequently,

the gross profit margin sizable incline to 17.7% (FY23: 13.2%). The incline is

attributable to improved sales and optimized cost of production. The operating

profit margin also inclined to 8% (FY23: 2.6%). The Finance cost of the Company

sizably inclines to PKR 434mln (FY23: 292mln). Thus, the Company’s net profit

clocked at PKR 114mln (FY23: PKR 124mln). with the net profit margin stood at

1.2% (FY23: 1.8%). The decline in net margin is due to the inclined taxation

cost (FY24: 195mln, FY23: PKR 101mln) due to the change in policy from shifting

from a final tax regime to normal tax regime. The management closely monitors

overheads, translating into an improvement in 1HFY25. Gross margin stood at 19%

and the operating profit margin of 8.4%. Hence, the net profit margin clocked at 1.3%.

Sustainability

In

line with improving the business environment, the Company has

installed 1MW of solar capacity to mitigate the risk of escalating energy costs.

The Company’s current energy cost-to-sale ratio stood at 6.1% which will be

improved going forward. The rating team further added that the Company intends

to add dyeing facility to its production plants

Financial Risk

Working capital

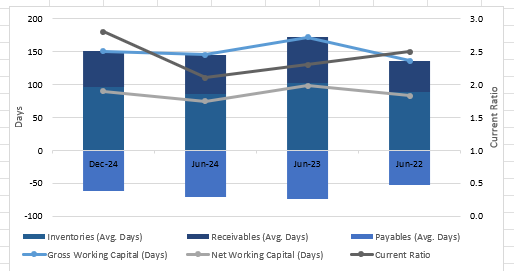

During FY24, the

Company’s net working capital days declined to 75 days (FY23: 98 days) due to a

decrease in inventory days (FY24: 86 days, FY23: PKR 102 days) and receivables

days (FY24: 59 days, FY23: 70 days). On the other hand, the Company’s

short-term trade leverage decreased and stood at 12.3% in FY24 (FY23: 14.3%)

and 24.9% during 1HFY25. During FY24, the current ratio of the Company is 2.1x

(FY23: 2.3x).

Coverages

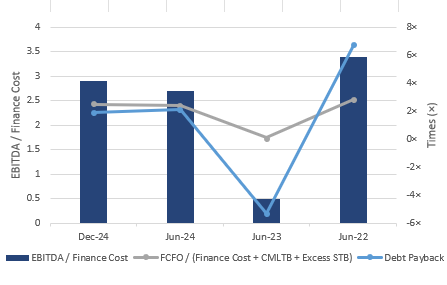

During FY24, the FCFO

of the Company sizably increased to PKR 956mln (FY23: PKR 28mln) due to an increase

in EBITDA. Consequently, the interest coverage ratio witnessed an incline to 2.4x

(FY23: 0.1x) as well as debt coverage ratio to 1.6x (FY23: 0.1x), despite the

increase in the finance cost (FY24: PKR 434mln, FY23: PKR 292mln). During 1HFY25, the Company’s FCFO clocked at PKR 439mln, while the interest coverage

and debt coverage ratio stood at 2.5x and 1.9x respectively.

Capitalization

During

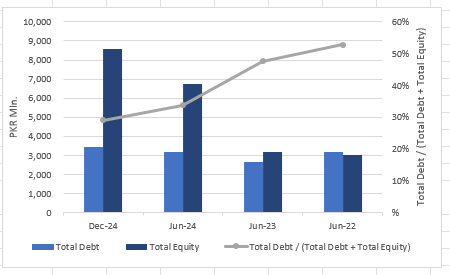

FY24, the Company’s leveraging itched down to 33.8% (FY23: 47.7%). Short-term

borrowings make up 66% of the total borrowings, increased to PKR 2,259mln in FY24

(FY23: 1,599mln) and the overall borrowings of the Company also reflected an

upward trend and clocked at PKR 3,196mln at the end of FY24 (FY23: PKR 2,645mln).

During FY24, the equity base of the company stood at PKR 6,727mln (FY23: PKR 3,153mln).

The incline in equity base is attributable to the recording of revaluation on

assets. During 1HFY25, the Company’s leveraging

stood at 29.1%.

|